Fintech

More and more neobanks are becoming mobile networks and Nubank wants in on the action

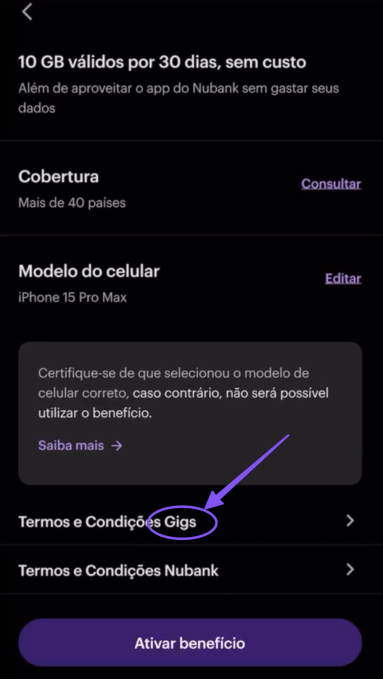

Nubank is taking its first steps into the realm of mobile networking, as Traded on the NYSE Brazilian neobank launches an eSIM (Built-in SIM) service for travellers. The service will give customers access to 10GB of free roaming internet in more than 40 countries without having to change their existing physical SIM or eSIM card.

The launch comes shortly after the news emerged first that the National Telecommunications Agency of Brazil (ANATEL) had given the green light to plans for Nubank to become a mobile virtual network operator (MVNO) in partnership with the wireless giant Clear. While the plan is still in the early stages and Nubank has not confirmed any of the launch details (the company also declined to comment for this article), we can now confirm that it is at least tiptoeing into the mobile network sphere – a trend in growth within the fintech fraternity.

Nubank CEO and Co-Founder David Vélez and his colleagues celebrate the company’s debut on the New York Stock Exchange in December 2021Image credits: NYSE (opens in new window)

From neobanks to neo-MVNOs

Neobanks, a new generation of financial institutions that serve as digitally native challengers to incumbent banking operators, follow in the footsteps of traditional banks by offering ancillary services to target new customers, such as budgeting tools, spending data and insights, and easy access to the stock market. While neobanks have increased in popularity, the same goes for the MVNO (virtual mobile network operator), driven by the rise of eSIM, cloud and the proliferation of third-party software that make all-digital distribution strategies a no-brainer.

Nubank sits at the intersection of these trends.

The Brazilian company, founded 10 years ago, has been in crisis of late, its valuation rising about 170% in the past year and hitting an all-time high of $58 billion in March. The company swung from a net loss of $9 million in 2022 to a net profit of $1 billion last yeara trend that will continue into 2024 record revenue in the first trimester e its net profit more than doubled on the corresponding period of the previous year. Nubank also passed by 100 million customers in its core markets of Brazil, Mexico and Colombia, where it operates a range of services including bank accounts, credit cards, loans, insurance, investments and, now, a mobile data service for travellers.

The new service is aimed at customers of Nubank Ultravioleta premium subscription launched three years ago with bundled benefits like insurance, higher credit limits, cashback, family accounts and more.

Last month, Nubank revealed that it was enter the travel industry with the upcoming launch of a new “global account”, in collaboration with Wise European fintech to offer Ultravioleta subscribers international money transfers at low rates. In this context, the company is now launching an eSIM service for those who own compatible smartphones, with 10 GB of data for travelers in the United States, Latin America and Europe. The eSIM is activated via the Nubank app, with the underlying infrastructure powered by Concertsa platform that gives budding mobile network providers everything they need via a single API, basically what Stripe has done in finance, but for mobile phone plans.

Gigs is backed by the likes of Gradient Ventures, Google’s early-stage venture capital arm, and Uber CEO Dara Khosrowshahi.

“Bundling of mobile plans represents a powerful lever for neobanks to turn irregular users into monthly paying subscribers, encourage upgrades to premium features, and create an ecosystem where banking serves as a hub for multiple value-added services,” co -founder and CEO of Gigs Herman Frank he told TechCrunch.

Activating the eSIM in the Nubank appImage credits: Nubank via Gigs

Activating the eSIM in the Nubank appImage credits: Nubank via Gigs

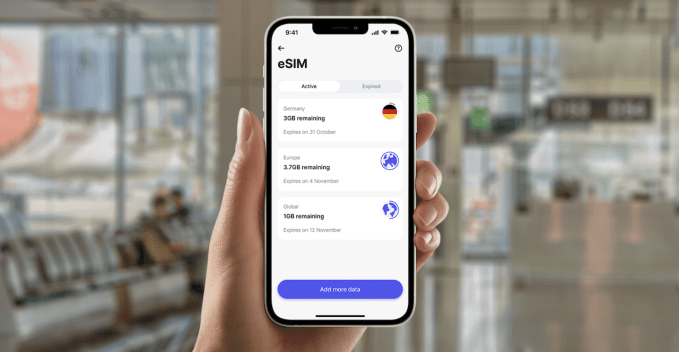

Nubank’s launch echoes movements elsewhere in the fintech fray. In February, Revolut-a $25 billion British neobank — has launched a similar eSIM service for premium subscribers. And last year, The Indian neobank Zolve Also added mobile networks to its arsenal of services so that immigrants can not only open their own banking system before arriving in the United States, but also have a mobile service also ready upon arrival.

This highlights the synergies between financial services and mobile communications: both are essential for people to function today, but both traditionally present similar barriers, particularly for those arriving in a country for the first time. We have seen operators launching banking services AS T-Mobile did it in the US with T-Mobile moneywhile traditional banks have also gone in the opposite direction, highlighted by the Brazilian Banco Inter AND Standard Bank in South Africa both have launched their own MVNO services.

“Our interaction with the bank today is already focused on our mobile number, both for the banking operations themselves and for security checks,” Allan T. Rasmussen, a telecommunications industry consultant, analyst and MVNO specialist told TechCrunch. “Mobile operators are entering the banking business, trying to become banks themselves, and traditional banks and fintechs are doing the same by becoming MVNOs.”

Revolut’s eSIM serviceImage credits: Revolution

Revolut’s eSIM serviceImage credits: Revolution

But neobanks, in particular, are synergistic with MVNOs: they are both “virtual”, with technology playing an important role in their respective offerings, often only with online support and account access. It’s also both marketed as having lower overhead, which gives them greater agility and ability to offer lower prices than incumbents. And as we’ve seen with Revolut and now Nubank, eSIMs are pushing this cross-pollination even further, as they compete for mindshare, revenue and access to customer data and touchpoints.

“To succeed as an MVNO, you need a distribution channel – this is the first test of your presentation to an operator,” James GreyCEO of telecommunications consultancy firm Gray stone strategy, he told TechCrunch. “Banks already have this with traditional banking services or through websites and apps. However, the recent move by Revolut – and I suspect other neobanks in the future – is interesting because these are not traditional organisations. Their whole job is to challenge the status quo and they are doing it very successfully in the banking sector, so why not a merger between banking and telecoms? They have the channels and the brand pull.”

MVN… no?

One small problem: neobanks are not actually positioning themselves as MVNOs with their new travel eSIM services. A Revolut spokesperson told TechCrunch in February: “Revolut is not becoming an MVNO but has partnered with 1Global which brings together many MVNOs and roaming access agreements into a single network to create a global footprint of the best operators.”

MVNOs are independent mobile services built on the operators’ infrastructure, and there are many different mobile virtual network enablers (MVNEs) and aggregators (MVNAs) on the market (such as 1Global) that help companies launch mobile networks, taking care of the provisioning of the SIM, billing and similar Like. While Revolut doesn’t offer voice and SMS, or assign a phone number, it still relies on the operator’s infrastructure via an MVNE to offer its own branded mobile data service, which looks a lot like Revolut becoming an MVNO.

But calling itself an MVNO may require additional regulatory scrutiny. While banks are already strictly regulated as financial institutions, being classified as a telecommunications company would likely result in additional regulatory obligations. This is something we’re seeing happen right now in the United States, with the Federal Communications Commission (FCC) trying to determine whether connected cars should be classified as MVNOsfollowing the a New York Times report about how connected cars are used by abusive partners to track down their victims.

While Nubank is indeed preparing to launch an MVNO service in its home country of Brazil, its travel eSIM service is easier to bring to market thanks to its partnership with Gigs, as that partner takes on all the regulatory compliance complexities that come with territory.

“Telecommunications is a highly regulated industry in all countries and a key part of Gigs’ end-to-end value proposition is that we eliminate all regulatory complexity for our customers,” Frank said. “To do this, Gigs almost always acts as a licensed carrier, meaning the burden of compliance falls on Gigs and not our customers. This allows our customers to launch their own mobile service, without legally becoming a provider in a regulated industry.”

Federal banking regulators have issued a statement reminding banks of the potential risks associated with third-party arrangements to provide bank deposit products and services.

The agencies support responsible innovation and banks that engage in these arrangements in a safe and fair manner and in compliance with applicable law. While these arrangements may offer benefits, supervisory experience has identified a number of safety and soundness, compliance, and consumer concerns with the management of these arrangements. The statement details potential risks and provides examples of effective risk management practices for these arrangements. Additionally, the statement reminds banks of existing legal requirements, guidance, and related resources and provides insights that the agencies have gained through their oversight. The statement does not establish new supervisory expectations.

Separately, the agencies requested additional information on a broad range of arrangements between banks and fintechs, including for deposit, payment, and lending products and services. The agencies are seeking input on the nature and implications of arrangements between banks and fintechs and effective risk management practices.

The agencies are considering whether to take additional steps to ensure that banks effectively manage the risks associated with these different types of arrangements.

SUBSCRIBE TO THE NEWSLETTER

And get exclusive articles on the stock markets

Exploring the complex landscape of global financial regulation, we gather insights from leading fintech leaders, including CEOs and finance experts. From the game-changing impact of PSD2 to the significant role of GDPR in data security, explore the four key regulatory changes that have reshaped fintech development, answering the question: “What changes in financial regulation have impacted fintech development?”

- PSD2 revolutionizes access to financial technology

- GDPR Improves Fintech Data Privacy

- Regulatory Sandboxes Drive Fintech Innovation

- GDPR Impacts Fintech Data Security

PSD2 revolutionizes access to financial technology

When it comes to regulatory impact on fintech development, nothing comes close to PSD2. This EU regulation has created a new level playing field for market players of all sizes, from fintech startups to established banks. It has had a ripple effect on other markets around the world, inspiring similar regulatory frameworks and driving global innovation in fintech.

The Payment Services Directive (PSD2), the EU law in force since 2018, has revolutionized the fintech industry by requiring banks to provide third-party payment providers (TPPs) with access to payment services and customer account information via open APIs. This has democratized access to financial data, fostering the development of personalized financial instruments and seamless payment solutions. Advanced security measures such as Strong Customer Authentication (SCA) have increased consumer trust, pushing both fintech companies and traditional banks to innovate and collaborate more effectively, resulting in a dynamic and consumer-friendly financial ecosystem.

The impact of PSD2 has extended beyond the EU, inspiring similar regulations around the world. Countries such as the UK, Australia and Canada have launched their own open banking initiatives, spurred by the benefits seen in the EU. PSD2 has highlighted the benefits of open banking, also prompting US financial institutions and fintech companies to explore similar initiatives voluntarily.

This has led to a global wave of fintech innovation, with financial institutions and fintech companies offering more integrated, personalized and secure services. The EU’s leadership in open banking through PSD2 has set a global standard, promoting regulatory harmonization and fostering an interconnected and innovative global financial ecosystem.

Looking ahead, the EU’s PSD3 proposals and Financial Data Access (FIDA) regulations promise to further advance open banking. PSD3 aims to refine and build on PSD2, with a focus on improving transaction security, fraud prevention, and integration between banks and TPPs. FIDA will expand data sharing beyond payment accounts to include areas such as insurance and investments, paving the way for more comprehensive financial products and services.

These developments are set to further enhance connectivity, efficiency and innovation in financial services, cementing open banking as a key component of the global financial infrastructure.

General Manager, Technology and Product Consultant Fintech, Insurtech, Miquido

GDPR Improves Fintech Data Privacy

Privacy and data protection have been taken to another level by the General Data Protection Regulation (GDPR), forcing fintech companies to tighten their data management. In compliance with the GDPR, organizations must ensure that personal data is processed fairly, transparently, and securely.

This has led to increased innovation in fintech towards technologies such as encryption and anonymization for data protection. GDPR was described as a top priority in the data protection strategies of 92% of US-based companies surveyed by PwC.

Financial Expert, Sterlinx Global

Regulatory Sandboxes Drive Fintech Innovation

Since the UK’s Financial Conduct Authority (FCA) pioneered sandbox regulatory frameworks in 2016 to enable fintech startups to explore new products and services, similar frameworks have been introduced in other countries.

This has reduced the “crippling effect on innovation” caused by a “one size fits all” regulatory approach, which would also require machines to be built to complete regulatory compliance before any testing. Successful applications within sandboxes give regulators the confidence to move forward and address gaps in laws, regulations, or supervisory approaches. This has led to widespread adoption of new technologies and business models and helped channel private sector dynamism, while keeping consumers protected and imposing appropriate regulatory requirements.

Co-founder, UK Linkology

GDPR Impacts Fintech Data Security

A big change in financial regulations that has had a real impact on fintech is the 2018 EU General Data Protection Regulation (GDPR). I have seen how GDPR has pushed us to focus more on user privacy and data security.

GDPR means we have to handle personal data much more carefully. At Leverage, we have had to step up our game to meet these new rules. We have improved our data encryption and started doing regular security audits. It was a little tricky at first, but it has made our systems much more secure.

For example, we’ve added features that give users more control over their data, like simple consent tools and clear privacy notices. These changes have helped us comply with GDPR and made our customers feel more confident in how we handle their information.

I believe that GDPR has made fintech companies, including us at Leverage, more transparent and secure. It has helped build trust with our users, showing them that we take data protection seriously.

CEO & Co-Founder, Leverage Planning

Related Articles

Application Programming Interface (API) Infrastructure Platform M2P Financial Technology has reached the final round to raise $80 million, at a valuation of $900 million.

Specifically, M2P Fintech, formerly known as Yap, is closing a new funding round involving new and existing investors, according to entrackr.com. The India-based company, which last raised funding two and a half years ago, previously secured $56 million in a round led by Insight Partners, earning a post-money valuation of $650 million.

A source indicated that M2P Fintech is ready to raise $80 million in this new funding round, led by a new investor. Existing backers, including Insight Partners, are also expected to participate. The new funding is expected to go toward enhancing the company’s technology infrastructure and driving growth in domestic and international markets.

What does M2P Fintech do?

M2P Fintech’s API platform enables businesses to provide branded financial services through partnerships with fintech companies while maintaining regulatory compliance. In addition to its operations in India, the company is active in Nepal, UAE, Australia, New Zealand, Philippines, Bahrain, Egypt, and many other countries.

Another source revealed that M2P Fintech’s valuation in this funding round is expected to be between USD 880 million and USD 900 million (post-money). The company has reportedly received a term sheet and the deal is expected to be publicly announced soon. The Tiger Global-backed company has acquired six companies to date, including Goals101, Syntizen, and BSG ITSOFT, to enhance its service offerings.

According to TheKredible, Beenext is the company’s largest shareholder with over 13% ownership, while the co-founders collectively own 34% of the company. Although M2P Fintech has yet to release its FY24 financials, it has reported a significant increase in operating revenue. However, this growth has also been accompanied by a substantial increase in losses.

By Gloria Methri

Today

- To come

- Aveni Assistance

- Aveni Detection

Artificial intelligence Financial Technology Aveni has announced one of the largest Series A investments in a Scottish company this year, amounting to £11 million. The investment is led by Puma Private Equity with participation from Par Equity, Lloyds Banking Group and Nationwide.

Aveni combines AI expertise with extensive financial services experience to create large language models (LLMs) and AI products designed specifically for the financial services industry. It is trusted by some of the UK’s leading financial services firms. It has seen significant business growth over the past two years through its conformity and productivity solutions, Aveni Detect and Aveni Assist.

This investment will enable Aveni to build on the success of its existing products, further consolidate its presence in the sector and introduce advanced technologies through FinLLM, a large-scale language model specifically for financial services.

FinLLM is being developed in partnership with new investors Lloyds Banking Group and Nationwide. It is a large, industry-aligned language model that aims to set the standard for transparent, responsible and ethical adoption of generative AI in UK financial services.

Following the investment, the team developing the FinLLM will be based at the Edinburgh Futures Institute, in a state-of-the-art facility.

Joseph Twigg, CEO of Aveniexplained, “The financial services industry doesn’t need AI models that can quote Shakespeare; it needs AI models that deliver transparency, trust, and most importantly, fairness. The way to achieve this is to develop small, highly tuned language models, trained on financial services data, and reviewed by financial services experts for specific financial services use cases. Generative AI is the most significant technological evolution of our generation, and we are in the early stages of adoption. This represents a significant opportunity for Aveni and our partners. The goal with FinLLM is to set a new standard for the controlled, responsible, and ethical adoption of generative AI, outperforming all other generic models in our select financial services use cases.”

Previous Article

Network International and Biz2X Sign Partnership for SME Financing

![]()

IBSi Daily News Analysis

SMBs Leverage Cloud to Gain Competitive Advantage, Study Shows

IBSi FinTech Magazine

![]()

- The Most Trusted FinTech Magazine Since 1991

- Digital monthly issue

- Over 60 pages of research, analysis, interviews, opinions and rankings

- Global coverage

subscribe now

Fred Thiel – The cryptocurrency market is flashing a signal that has never flashed before

Jeff Booth – “We are entering a storm for which nobody is prepared!”

“Altcoin’s season has officially started – here’s what will come after” – Ric Edelman

“I just became 100% more bullish on BTC and these cryptocurrencies – Tom Lee

When Bitcoin hits this price, the Internet will not survive – Catie Wood

DeFi Technologies Appoints Andrew Forson to Board of Directors

US Agencies Request Information on Bank-Fintech Dealings

Block Investors Need More to Assess Crypto Unit’s Earnings Potential, Analysts Say — TradingView News

Switchboard Revolutionizes DeFi with New Oracle Aggregator

Is Zypto Wallet a Reliable Choice for DeFi Users?

Fred Thiel – The cryptocurrency market is flashing a signal that has never flashed before

Jeff Booth – “We are entering a storm for which nobody is prepared!”

“Altcoin’s season has officially started – here’s what will come after” – Ric Edelman

“I just became 100% more bullish on BTC and these cryptocurrencies – Tom Lee

When Bitcoin hits this price, the Internet will not survive – Catie Wood

-

DeFi12 months ago

DeFi12 months agoDeFi Technologies Appoints Andrew Forson to Board of Directors

-

Fintech12 months ago

Fintech12 months agoUS Agencies Request Information on Bank-Fintech Dealings

-

News1 year ago

News1 year agoBlock Investors Need More to Assess Crypto Unit’s Earnings Potential, Analysts Say — TradingView News

-

DeFi12 months ago

DeFi12 months agoSwitchboard Revolutionizes DeFi with New Oracle Aggregator

-

DeFi12 months ago

DeFi12 months agoIs Zypto Wallet a Reliable Choice for DeFi Users?

-

News1 year ago

News1 year agoBitcoin and Technology Correlation Collapses Due to Excess Supply

-

Fintech12 months ago

Fintech12 months agoWhat changes in financial regulation have impacted the development of financial technology?

-

Fintech12 months ago

Fintech12 months agoScottish financial technology firm Aveni secures £11m to expand AI offering

-

Fintech12 months ago

Fintech12 months agoScottish financial technology firm Aveni raises £11m to develop custom AI model for financial services

-

News1 year ago

News1 year agoValueZone launches new tools to maximize earnings during the ongoing crypto summer

-

Videos6 months ago

Videos6 months ago“Artificial intelligence is bringing us to a future that we may not survive” – Sco to Whitney Webb’s Waorting!

-

DeFi1 year ago

DeFi1 year agoTON Network Surpasses $200M TVL, Boosted by Open League and DeFi Growth ⋆ ZyCrypto