Fintech

Partnerships and Collaborations, Innovation and CX, Growth of Fintech, Open Banking, Large Start-ups

![]()

Company logo

Swiss market for embedded finance business and investment opportunities

Swiss market for embedded finance business and investment opportunities

Dublin, May 21, 2024 (GLOBE NEWSWIRE) — The “Swiss Integrated Finance Business and Investment Opportunity Data – 75+ KPIs across Integrated Lending, Insurance, Payments and Wealth Segments – Q1 2024 Update” report has been added ResearchAndMarkets.com offer.

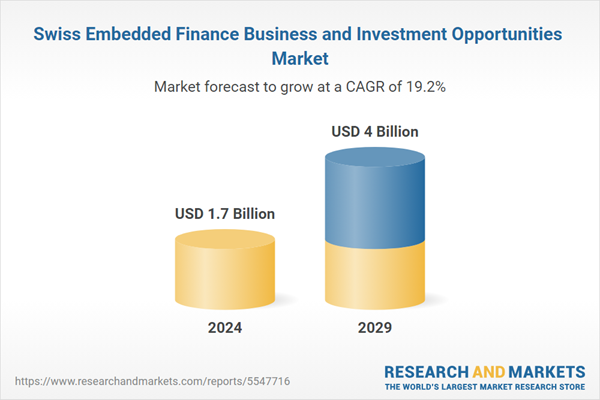

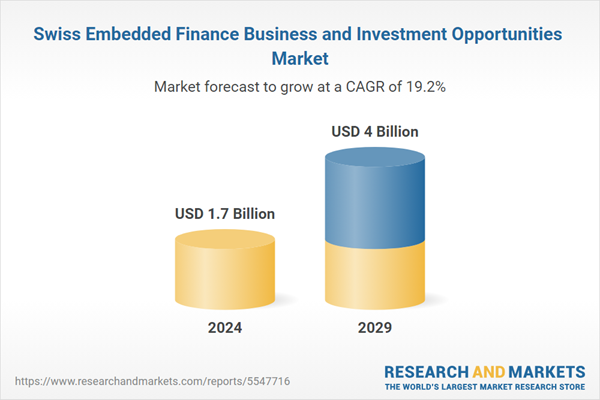

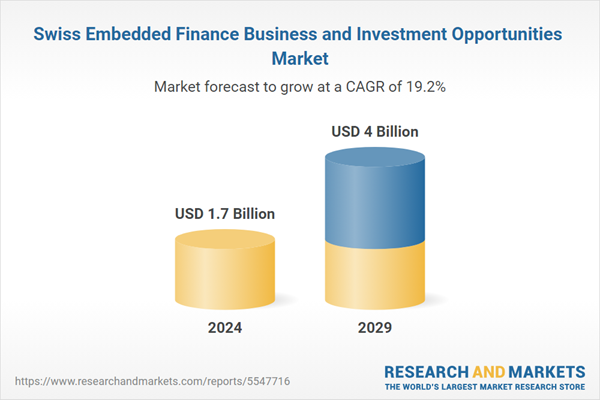

The integrated finance sector in Switzerland is expected to grow by 26.9% year-on-year to reach $1.67 billion in 2024.

The integrated finance sector is expected to grow steadily over the forecast period, registering a CAGR of 19.2% during 2024-2029. Integrated financial revenues in the country will increase from $1.67 billion in 2024 to $4.04 billion by 2029.

Key Drivers of the Swiss Embedded Finance Market: Switzerland has a well-established banking sector, known for its stability and confidentiality. Traditional banks are gradually adapting to the digital age by offering online and mobile banking services. However, the pace of innovation has been relatively slower than in fintech hubs such as the UK or US.

-

Innovation and Customer Experience: Embedded Finance seamlessly integrates financial services within existing platforms, offering a convenient and frictionless customer experience. This resonates with the tech-savvy Swiss population, driving adoption.

-

Fintech growth: Switzerland boasts a thriving fintech ecosystem, promoting collaboration between traditional banks and innovative startups. This synergy fuels the development and implementation of integrated financial solutions.

-

Dubai’s largest lender, Emirates NBD, has made an equity investment in trade finance and treasury network Komgo. The company currently claims to have 10,000 business users worldwide and a daily transaction processing value of $1 billion.

-

Partnerships and collaborations: Integrated finance often thrives through partnerships between fintech startups, traditional financial institutions, and non-financial companies such as e-commerce platforms, marketplaces, and ride-sharing services. These collaborations enable the integration of financial services into consumers’ everyday experiences.

-

In February 2024, a historic agreement was signed between Switzerland and Panama, marking a significant step forward in the fight against financial crimes, including money laundering, terrorist financing and corruption.

Latest innovations in the integrated finance sector in Switzerland

Integrated Insurance: The integration of tailored insurance products within specific workflows is gaining traction. For example, integrated travel insurance offered within travel booking platforms. In October 2023, additiv, a global leader in integrated finance, announced that it will support Coop in the launch of Coop Finance+, a new comprehensive app for integrated financial services. At launch, Coop Finance+ offers individual banking products and pension solutions, with plans to further expand in the coming months. Services are provided by Hypothekarbank Lenzburg for banking and by Vanguard, OLZ, Liberty Vorsorge and Glarner Kantonalbank for pensions.

The story continues

-

Open Banking: Open banking regulations allow for secure data sharing between financial institutions and third-party providers. This facilitates the development of innovative integrated financial solutions.

-

Artificial Intelligence (AI) and Machine Learning (ML): These technologies are used for risk assessment, fraud detection and personalized financial product recommendations within integrated financial platforms. There have never been more active companies in the Swiss fintech sector, which numbered over 500 at the end of the first quarter of 2024.

-

Large Swiss Startups Embedded Finance: In 2022, Zug-based tech startups raised around CHF 250 million in venture capital funding, making them the second largest recipient of fintech investments that year. The canton is widely known as the “Crypto Valley”, due to the high number of startups specializing in blockchain technology and cryptocurrencies located in the canton, including prominent industry names such as the Ethereum Foundation and Amina Bank, formerly known as SEBA Bank. and Bitcoin Suisse.

Key Attributes:

|

Report attribute |

Details |

|

No. of pages |

130 |

|

Forecast period |

2024-2029 |

|

Estimated market value (USD) in 2024 |

$1.7 billion |

|

Expected market value (USD) by 2029 |

$4 billion |

|

Annual compound growth rate |

19.2% |

|

Regions covered |

Swiss |

Scope

Size and forecasts of the Swiss embedded finance market

Integrated finance for key sectors

-

See retail

-

logistics

-

Telecommunications

-

Production

-

Consumer health

-

Others

Integrated finance by business model

-

Platforms

-

Enabler

-

Regulatory body

Integrated finance for distribution model

-

Own platforms

-

Third Party Platforms

Size and forecasts of the integrated insurance market in Switzerland

Integrated insurance by sector

-

Insurance integrated into consumer products

-

Integrated travel and hospitality insurance

-

Integrated insurance in the automotive sector

-

Integrated health insurance

-

Integrated insurance in the real estate sector

-

Integrated insurance in transport and logistics

-

Insurance incorporated into others

Integrated insurance for consumer segments

Integrated insurance by type of offer

Integrated insurance for business model

-

Platforms

-

Enabler

-

Regulatory body

Integrated insurance for distribution model

-

Own platforms

-

Third Party Platforms

Integrated insurance by distribution channel

-

Integrated sales

-

Bancassurance

-

Brokers/IFAs

-

Bonded agents

Integrated insurance by insurance type

Integrated insurance in the Non-Life segment

Size and forecasts of the integrated lending market in Switzerland

Integrated loans for consumer segments

-

Business loan

-

Retail lending

Integrated loans for B2B sectors

-

Integrated lending in retail and consumer goods

-

Lending integrated into IT and software services

-

Integrated lending in media, entertainment and leisure

-

Integrated loans in the manufacturing and distribution sector

-

Integrated loans in the real estate sector

-

Loan incorporated into Other

Integrated lending by B2C sectors

-

Loan integrated into retail purchases

-

Loan incorporated into home improvement

-

Integrated loans in the leisure and entertainment sector

-

Loan embedded in the healthcare and wellness sector

-

Loan incorporated into Other

Loan incorporated by type

-

BNPL loans

-

POS loan

-

Personal loans

Integrated loans for business model

-

Platforms

-

Enabler

-

Regulatory body

Integrated loans for distribution model

-

Own platforms

-

Third Party Platforms

Size and forecasts of the embedded payments market in Switzerland

Embedded payment for consumer segments

Integrated payment by end-use sector

-

Integrated payment in the retail and consumer goods sector

-

Payment integrated into digital products and services

-

Payment incorporated into bill payments

-

Integrated payment in travel and hospitality

-

Integrated payment in the leisure and entertainment sector

-

Payment integrated into health and well-being

-

Payment integrated into office supplies and equipment

-

Payment embedded in More

Built-in payment for business model

-

Platforms

-

Enabler

-

Regulatory body

Built-in payment per distribution model

-

Own platforms

-

Third Party Platforms

Size and forecast of the Swiss embedded asset management market

Market size and forecast of the asset-based financial management sector in Switzerland

Asset-based finance by asset type

Asset-based finance by end users

For more information on this report, visit https://www.researchandmarkets.com/r/fig0fr

About ResearchAndMarkets.com

ResearchAndMarkets.com is the world’s leading source of international market research reports and market data. We provide you with the latest data on international and regional markets, key industries, top companies, new products and the latest trends.

Attached

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood,Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./ CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900

Federal banking regulators have issued a statement reminding banks of the potential risks associated with third-party arrangements to provide bank deposit products and services.

The agencies support responsible innovation and banks that engage in these arrangements in a safe and fair manner and in compliance with applicable law. While these arrangements may offer benefits, supervisory experience has identified a number of safety and soundness, compliance, and consumer concerns with the management of these arrangements. The statement details potential risks and provides examples of effective risk management practices for these arrangements. Additionally, the statement reminds banks of existing legal requirements, guidance, and related resources and provides insights that the agencies have gained through their oversight. The statement does not establish new supervisory expectations.

Separately, the agencies requested additional information on a broad range of arrangements between banks and fintechs, including for deposit, payment, and lending products and services. The agencies are seeking input on the nature and implications of arrangements between banks and fintechs and effective risk management practices.

The agencies are considering whether to take additional steps to ensure that banks effectively manage the risks associated with these different types of arrangements.

SUBSCRIBE TO THE NEWSLETTER

And get exclusive articles on the stock markets

Exploring the complex landscape of global financial regulation, we gather insights from leading fintech leaders, including CEOs and finance experts. From the game-changing impact of PSD2 to the significant role of GDPR in data security, explore the four key regulatory changes that have reshaped fintech development, answering the question: “What changes in financial regulation have impacted fintech development?”

- PSD2 revolutionizes access to financial technology

- GDPR Improves Fintech Data Privacy

- Regulatory Sandboxes Drive Fintech Innovation

- GDPR Impacts Fintech Data Security

PSD2 revolutionizes access to financial technology

When it comes to regulatory impact on fintech development, nothing comes close to PSD2. This EU regulation has created a new level playing field for market players of all sizes, from fintech startups to established banks. It has had a ripple effect on other markets around the world, inspiring similar regulatory frameworks and driving global innovation in fintech.

The Payment Services Directive (PSD2), the EU law in force since 2018, has revolutionized the fintech industry by requiring banks to provide third-party payment providers (TPPs) with access to payment services and customer account information via open APIs. This has democratized access to financial data, fostering the development of personalized financial instruments and seamless payment solutions. Advanced security measures such as Strong Customer Authentication (SCA) have increased consumer trust, pushing both fintech companies and traditional banks to innovate and collaborate more effectively, resulting in a dynamic and consumer-friendly financial ecosystem.

The impact of PSD2 has extended beyond the EU, inspiring similar regulations around the world. Countries such as the UK, Australia and Canada have launched their own open banking initiatives, spurred by the benefits seen in the EU. PSD2 has highlighted the benefits of open banking, also prompting US financial institutions and fintech companies to explore similar initiatives voluntarily.

This has led to a global wave of fintech innovation, with financial institutions and fintech companies offering more integrated, personalized and secure services. The EU’s leadership in open banking through PSD2 has set a global standard, promoting regulatory harmonization and fostering an interconnected and innovative global financial ecosystem.

Looking ahead, the EU’s PSD3 proposals and Financial Data Access (FIDA) regulations promise to further advance open banking. PSD3 aims to refine and build on PSD2, with a focus on improving transaction security, fraud prevention, and integration between banks and TPPs. FIDA will expand data sharing beyond payment accounts to include areas such as insurance and investments, paving the way for more comprehensive financial products and services.

These developments are set to further enhance connectivity, efficiency and innovation in financial services, cementing open banking as a key component of the global financial infrastructure.

General Manager, Technology and Product Consultant Fintech, Insurtech, Miquido

GDPR Improves Fintech Data Privacy

Privacy and data protection have been taken to another level by the General Data Protection Regulation (GDPR), forcing fintech companies to tighten their data management. In compliance with the GDPR, organizations must ensure that personal data is processed fairly, transparently, and securely.

This has led to increased innovation in fintech towards technologies such as encryption and anonymization for data protection. GDPR was described as a top priority in the data protection strategies of 92% of US-based companies surveyed by PwC.

Financial Expert, Sterlinx Global

Regulatory Sandboxes Drive Fintech Innovation

Since the UK’s Financial Conduct Authority (FCA) pioneered sandbox regulatory frameworks in 2016 to enable fintech startups to explore new products and services, similar frameworks have been introduced in other countries.

This has reduced the “crippling effect on innovation” caused by a “one size fits all” regulatory approach, which would also require machines to be built to complete regulatory compliance before any testing. Successful applications within sandboxes give regulators the confidence to move forward and address gaps in laws, regulations, or supervisory approaches. This has led to widespread adoption of new technologies and business models and helped channel private sector dynamism, while keeping consumers protected and imposing appropriate regulatory requirements.

Co-founder, UK Linkology

GDPR Impacts Fintech Data Security

A big change in financial regulations that has had a real impact on fintech is the 2018 EU General Data Protection Regulation (GDPR). I have seen how GDPR has pushed us to focus more on user privacy and data security.

GDPR means we have to handle personal data much more carefully. At Leverage, we have had to step up our game to meet these new rules. We have improved our data encryption and started doing regular security audits. It was a little tricky at first, but it has made our systems much more secure.

For example, we’ve added features that give users more control over their data, like simple consent tools and clear privacy notices. These changes have helped us comply with GDPR and made our customers feel more confident in how we handle their information.

I believe that GDPR has made fintech companies, including us at Leverage, more transparent and secure. It has helped build trust with our users, showing them that we take data protection seriously.

CEO & Co-Founder, Leverage Planning

Related Articles

Application Programming Interface (API) Infrastructure Platform M2P Financial Technology has reached the final round to raise $80 million, at a valuation of $900 million.

Specifically, M2P Fintech, formerly known as Yap, is closing a new funding round involving new and existing investors, according to entrackr.com. The India-based company, which last raised funding two and a half years ago, previously secured $56 million in a round led by Insight Partners, earning a post-money valuation of $650 million.

A source indicated that M2P Fintech is ready to raise $80 million in this new funding round, led by a new investor. Existing backers, including Insight Partners, are also expected to participate. The new funding is expected to go toward enhancing the company’s technology infrastructure and driving growth in domestic and international markets.

What does M2P Fintech do?

M2P Fintech’s API platform enables businesses to provide branded financial services through partnerships with fintech companies while maintaining regulatory compliance. In addition to its operations in India, the company is active in Nepal, UAE, Australia, New Zealand, Philippines, Bahrain, Egypt, and many other countries.

Another source revealed that M2P Fintech’s valuation in this funding round is expected to be between USD 880 million and USD 900 million (post-money). The company has reportedly received a term sheet and the deal is expected to be publicly announced soon. The Tiger Global-backed company has acquired six companies to date, including Goals101, Syntizen, and BSG ITSOFT, to enhance its service offerings.

According to TheKredible, Beenext is the company’s largest shareholder with over 13% ownership, while the co-founders collectively own 34% of the company. Although M2P Fintech has yet to release its FY24 financials, it has reported a significant increase in operating revenue. However, this growth has also been accompanied by a substantial increase in losses.

By Gloria Methri

Today

- To come

- Aveni Assistance

- Aveni Detection

Artificial intelligence Financial Technology Aveni has announced one of the largest Series A investments in a Scottish company this year, amounting to £11 million. The investment is led by Puma Private Equity with participation from Par Equity, Lloyds Banking Group and Nationwide.

Aveni combines AI expertise with extensive financial services experience to create large language models (LLMs) and AI products designed specifically for the financial services industry. It is trusted by some of the UK’s leading financial services firms. It has seen significant business growth over the past two years through its conformity and productivity solutions, Aveni Detect and Aveni Assist.

This investment will enable Aveni to build on the success of its existing products, further consolidate its presence in the sector and introduce advanced technologies through FinLLM, a large-scale language model specifically for financial services.

FinLLM is being developed in partnership with new investors Lloyds Banking Group and Nationwide. It is a large, industry-aligned language model that aims to set the standard for transparent, responsible and ethical adoption of generative AI in UK financial services.

Following the investment, the team developing the FinLLM will be based at the Edinburgh Futures Institute, in a state-of-the-art facility.

Joseph Twigg, CEO of Aveniexplained, “The financial services industry doesn’t need AI models that can quote Shakespeare; it needs AI models that deliver transparency, trust, and most importantly, fairness. The way to achieve this is to develop small, highly tuned language models, trained on financial services data, and reviewed by financial services experts for specific financial services use cases. Generative AI is the most significant technological evolution of our generation, and we are in the early stages of adoption. This represents a significant opportunity for Aveni and our partners. The goal with FinLLM is to set a new standard for the controlled, responsible, and ethical adoption of generative AI, outperforming all other generic models in our select financial services use cases.”

Previous Article

Network International and Biz2X Sign Partnership for SME Financing

![]()

IBSi Daily News Analysis

SMBs Leverage Cloud to Gain Competitive Advantage, Study Shows

IBSi FinTech Magazine

![]()

- The Most Trusted FinTech Magazine Since 1991

- Digital monthly issue

- Over 60 pages of research, analysis, interviews, opinions and rankings

- Global coverage

subscribe now

Forget the CBDC! This is the greatest threat to your financial freedom: Whitney Webb and Mark Goodwin

“Final warning! I won’t say it anymore!” – Michael Saylor 2025 Bitcoin forecast

Fred Thiel – The cryptocurrency market is flashing a signal that has never flashed before

Jeff Booth – “We are entering a storm for which nobody is prepared!”

“Altcoin’s season has officially started – here’s what will come after” – Ric Edelman

DeFi Technologies Appoints Andrew Forson to Board of Directors

US Agencies Request Information on Bank-Fintech Dealings

Block Investors Need More to Assess Crypto Unit’s Earnings Potential, Analysts Say — TradingView News

Switchboard Revolutionizes DeFi with New Oracle Aggregator

Is Zypto Wallet a Reliable Choice for DeFi Users?

Forget the CBDC! This is the greatest threat to your financial freedom: Whitney Webb and Mark Goodwin

“Final warning! I won’t say it anymore!” – Michael Saylor 2025 Bitcoin forecast

Fred Thiel – The cryptocurrency market is flashing a signal that has never flashed before

Jeff Booth – “We are entering a storm for which nobody is prepared!”

“Altcoin’s season has officially started – here’s what will come after” – Ric Edelman

-

DeFi12 months ago

DeFi12 months agoDeFi Technologies Appoints Andrew Forson to Board of Directors

-

Fintech12 months ago

Fintech12 months agoUS Agencies Request Information on Bank-Fintech Dealings

-

News1 year ago

News1 year agoBlock Investors Need More to Assess Crypto Unit’s Earnings Potential, Analysts Say — TradingView News

-

DeFi12 months ago

DeFi12 months agoSwitchboard Revolutionizes DeFi with New Oracle Aggregator

-

DeFi12 months ago

DeFi12 months agoIs Zypto Wallet a Reliable Choice for DeFi Users?

-

News1 year ago

News1 year agoBitcoin and Technology Correlation Collapses Due to Excess Supply

-

Fintech12 months ago

Fintech12 months agoWhat changes in financial regulation have impacted the development of financial technology?

-

Fintech12 months ago

Fintech12 months agoScottish financial technology firm Aveni secures £11m to expand AI offering

-

Fintech12 months ago

Fintech12 months agoScottish financial technology firm Aveni raises £11m to develop custom AI model for financial services

-

News1 year ago

News1 year agoValueZone launches new tools to maximize earnings during the ongoing crypto summer

-

Videos6 months ago

Videos6 months ago“Artificial intelligence is bringing us to a future that we may not survive” – Sco to Whitney Webb’s Waorting!

-

DeFi1 year ago

DeFi1 year agoTON Network Surpasses $200M TVL, Boosted by Open League and DeFi Growth ⋆ ZyCrypto