Fintech

Block: 3 Reasons to Buy This Fintech Now (NYSE:SQ)

andresr

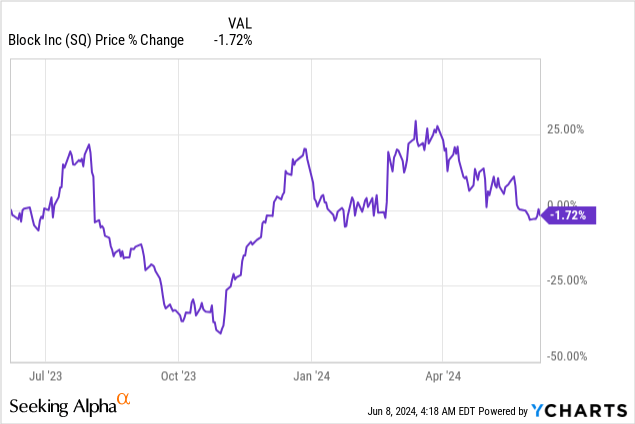

Block (NYSE:m2) remains a very attractive growth play for Fintech investors in fiscal 2024 as it sees continued gross earnings momentum across both core business segments, is benefiting from strong Cash App Card adoption and the most recent downtrend in the valuation makes the shares attractive from a valuation point of even seeing. Block shares have continued to sell off following Fintech’s solid Q1 2024 earnings, and I believe the drop represents a new engagement opportunity for long-term investors looking to increase their exposure to the fast-growing sector!

Previous rating

In my last article on Block I indicated that Fintech was doing a great job growing its gross profits across the board, but especially in Cash App, and that the profitability picture continued to improve: The blowout guidance makes this Fintech a strong buy. Block performed very well in this regard in the fiscal first quarter, but it retains considerable growth and upside potential in the Fintech market as it attracts more Cash App Card users. Block’s growth also compares favorably with that of PayPal (PYPL), which is struggling to keep customers on its payment platform.

Strong growth with significant earnings momentum

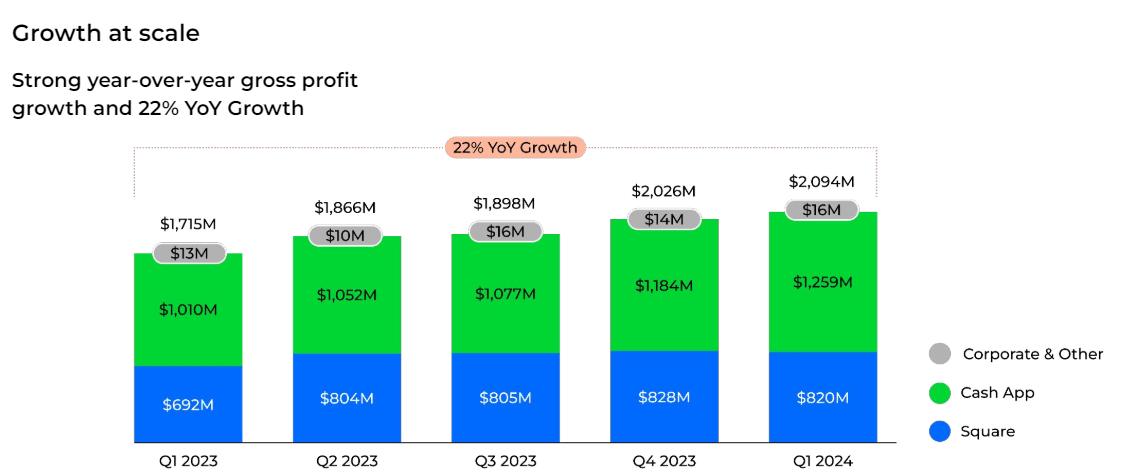

In the past, I’ve indicated that Block had considerable potential in the Fintech space due to the company’s aggressive scaling of its Cash App, which was essentially where all the momentum for Block was. In the latest quarter, Q1’24, Cash App’s gross earnings grew 25% year-over-year to a record $1.26 billion, while Square, which includes the fintech’s point-of-sale payment services , recorded 19% year-over-year growth to $820. M. While both segments clearly have momentum due to user growth (in Cash App) and growing product adoption (Square), Cash App remains the fastest growing and most important business segment for Block, and it is unlikely that this will change in the future.

To block

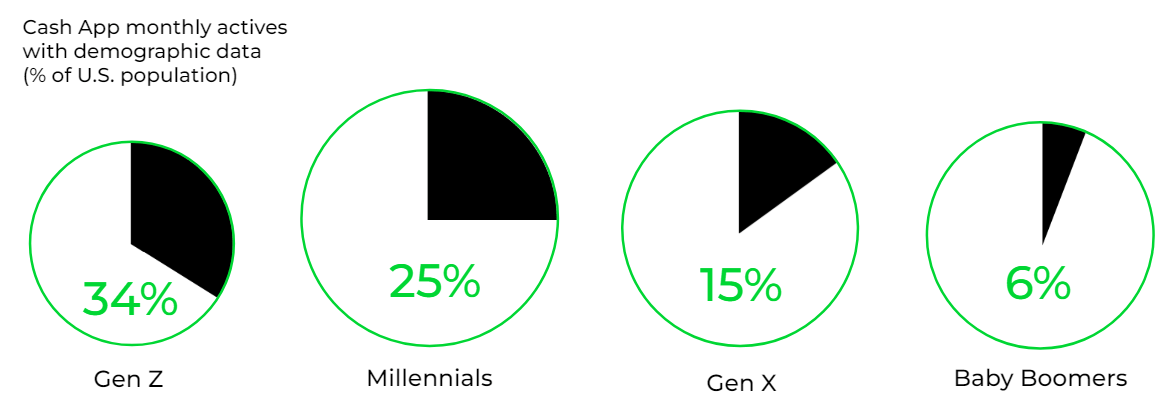

Cash App still has significant growth potential, as Block estimates the company only penetrates about 20% of the market. Generation Z and Millennials, who are Cash App’s most prolific users, represent a huge growth opportunity for Block in the coming years, and the company’s Cash App Card could be the product that attracts them.

To block

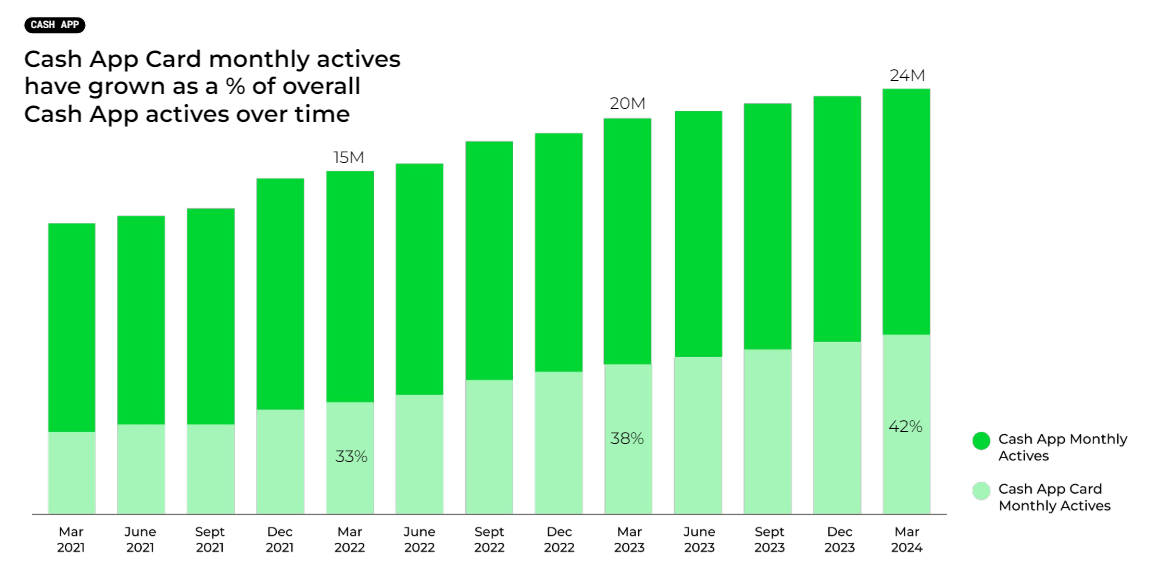

A key product for Block is the Cash App Card, which is a customizable debit card that can be used both online and in stores. The Cash App Card is connected to the Cash App and therefore allows easy and immediate money transfers, which is especially appreciated by younger users. This financial product is experiencing constant growth and currently has 24 million assets and growing usage.

To block

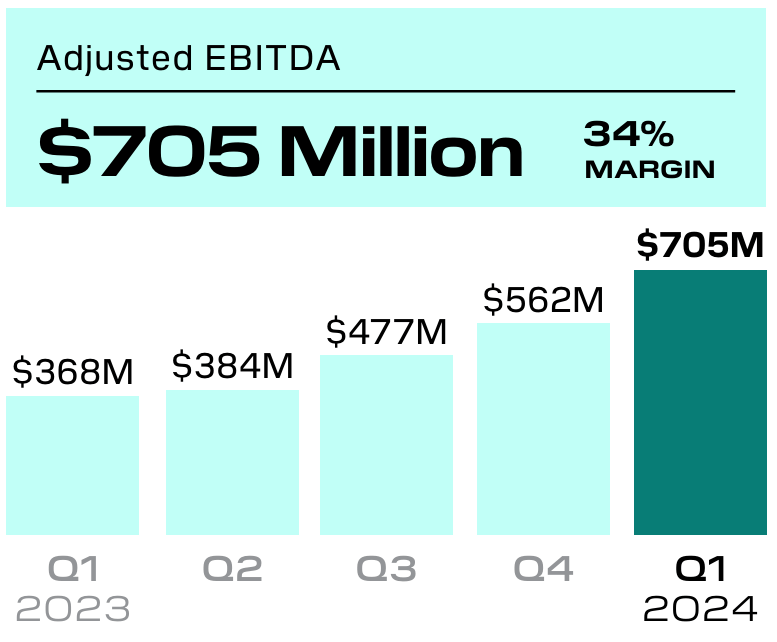

Cash App is primarily driving Block’s adjusted EBITDA gains in recent quarters. In the first quarter of 2024, the Fintech sector reported EBITDA growth of 92% year-over-year to $705 million, as well as significant expansion in EBITDA margins. In the previous quarter, Block posted an adjusted EBITDA margin of just 24%, so the fintech generated a quarterly gain of 10 PP in its most important metric.

To block

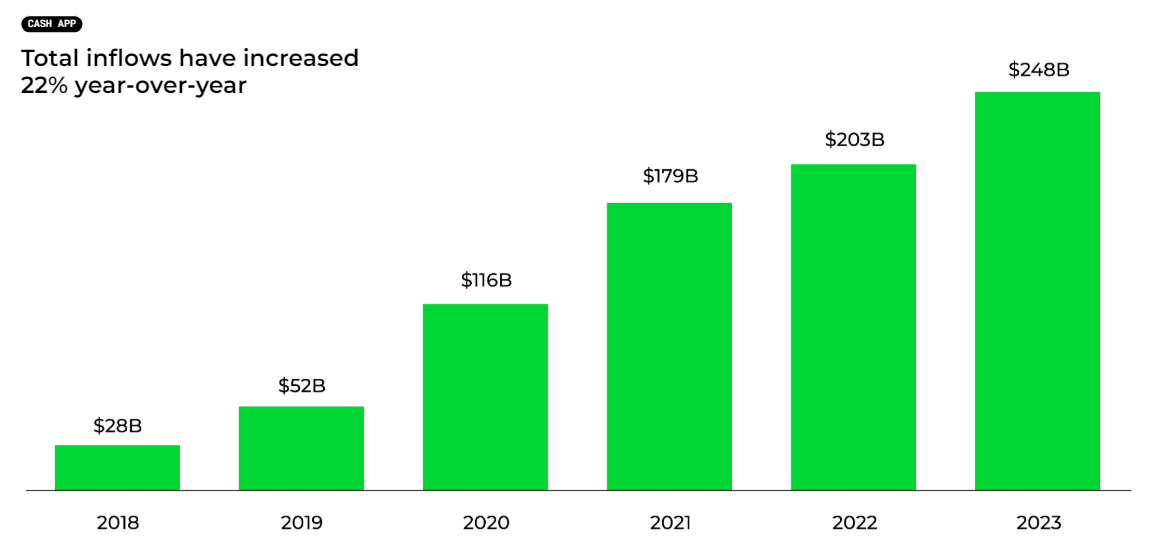

More money flows to Cash App. Millennials and Gen Z are responsible for 70% of cash inflows from Cash App as they tend to use the app more and are set to become the driving force of incremental cash flows in the future. In fiscal 2023, Block’s Cash App recorded inflows of $248 billion, showing 22% year-over-year growth. In 1Q24, Cash App inflows were $71 billion, growing 17% year over year. With more money flowing to Cash App (and greater app adoption), the ecosystem and the Cash App Card only become more attractive to users.

To block

3 catalysts for an upward revaluation

I see 3 specific catalysts for an upward revaluation of the stock price in fiscal 2024 and beyond:

- Continued growth in Cash App Card growth (both in terms of users and usage)

- Block is now consistently profitable on an adjusted EBITDA basis. I expect Fintech to be able to increase its EBITDA margins as it acquires more Millennial and Gen Z users

- The growth of incoming cash flows could make Cash App a very viable alternative to other payment services, including those offered by PayPal.

Block’s assessment

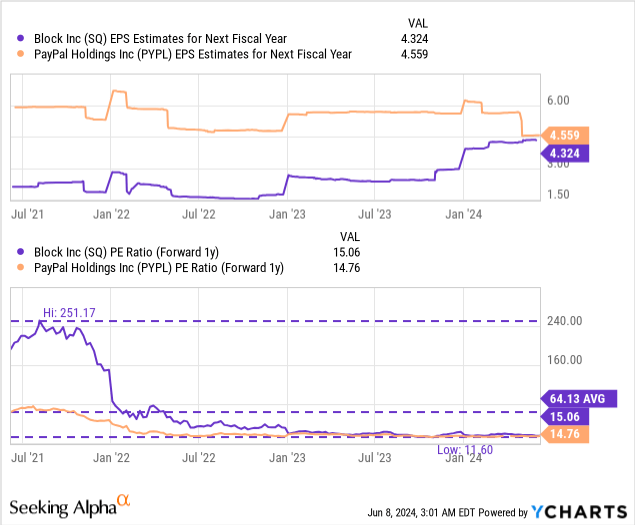

The good news from Block is that the fintech is already profitable, not just on an adjusted EBITDA basis, but also on a net profit basis. Therefore, Block can be valued using a traditional price-to-earnings ratio. The Fintech is currently valued at a P/E ratio of 15.1X which compares, for example, to a P/E ratio of 14.8X for PayPal, which is a key rival to Block in the Fintech space. Both Block and PayPal have traded at significantly higher P/E ratios in the past, especially during the pandemic, and Block is currently priced much lower than its long-term (3-year) average P/E ratio of 64.1X. PayPal’s 3-year average P/E ratio is 25.8X, so both PayPal and Block are trading significantly below their historical valuation averages. In PayPal’s case, I think this valuation cut is a little more deserved, but Block is doing well and growing much faster: Block is seeing annual EPS growth rates above 20% (through fiscal 2027 ).

As I indicated above, PayPal has fundamental problems remain relevant with its payment processing services, which has been reflected in an erosion of its customer base. Over the past year, PayPal has been almost constantly losing customers, leading to subdued EPS growth expectations for the fintech. PayPal is expected to grow its EPS by just 11% next year, which may be an optimistic estimate considering the company is still losing customers.

Block, on the other hand, is expected to continue growing in double digits (+28% y/y in fiscal 2025), which explains why I see Fintech as a very attractive alternative to PayPal… which essentially does trading at the same valuation multiplier. In my latest work on Block I stated that improving profitability and Cash App momentum are the reasons I see a fair value P/E ratio of 25X, which has not changed. With a consensus EPS estimate of $4.32 for fiscal 2025, Block has a fair value near $108 and significant appreciation potential… if Fintech continues to perform well.

Risks with Blocking

There are a number of risks that could affect how I view an investment in Block. If Fintech continues to grow its gross profits by double digits while improving its EBITDA, then I would be very happy to hold on to Block for a long time. What would change minds, however, is if Block fails to expand its EBITDA margins or if the Fintech sees a noticeable slowdown in growth in its high-performing Cash App business. Slowing Cash App Card adoption rates would also be a reason to reevaluate the investment thesis.

Final thoughts

Block remains a compelling growth story in the Fintech sector, especially since PayPal’s growth problems contrast well with and benefit Block. Fintech generated notable gross profit growth last quarter, primarily driven by growth in the Cash App segment. I believe Block’s profit explosion in fiscal 2024 indicates strong potential for EBITDA margin expansion, driven primarily by two groups of people: Millennials and Gen Z users. The stock is a bargain, in my opinion, and Block has the growth to support this valuation. I believe the risk profile for long-term investors in the Fintech market is still very attractive and I see continued upside in appreciation if Block continues to execute its growth strategy well, especially in Cash App!