Fintech

Claim and Lock: Goldman Sachs Selects the Best Fintech Stocks to Buy

In recent years, the financial industry has evolved significantly, driven by the emergence of fintech applications. These platforms, such as digital payment systems and peer-to-peer lending, have introduced more transparent and secure methods of transactions. As a result, consumer trust in these technologies has increased significantly, and companies are reaping the benefits of increased convenience and improved customer connectivity.

The fintech sector is large and continues to expand rapidly. Last year, the global fintech market was valued at nearly $295 billion, with projections indicating it will rise to $340 billion this year. According to Fortune Business Insights, the industry could reach $1.15 trillion by 2032, reflecting a compound annual growth rate (CAGR) of 16.5%.

In this dynamic environment, Goldman Sachs analyst Michael Ng has been closely monitoring the fintech sector and has identified two stocks, Affirm (NASDAQ:AFRM) and Block (NYSE:SQ), as major investment opportunities. Let’s see what these names have that sets them apart from the crowd.

Affirm holdings

At the top is Affirm Holdings, a customer-facing fintech dedicated to providing honest financial products to make your life easier. The company specializes in digital payments, providing a platform for digital and e-commerce use. Affirm offers several options for making payments in physical locations, including smartphone apps or the Affirm debit card. While the service works like a credit card, and can be used like one, there is a difference: Affirm users agree to their debt limit upfront, ensuring spending stays within affordable limits.

Affirm doesn’t charge users fees for the service, a move that helps keep the account transparent. The majority of Affirm’s revenue comes from commissions charged to sellers. This creates a win-win situation, as sellers benefit from guaranteed payment clearing through Affirm.

The result is that Affirm has long been at the forefront of “buy now, pay later” online apps. This positioning helped the company immensely during the pandemic period, when lockdown policies had the unintended ripple effect of boosting e-commerce and online payment systems.

However, as the pandemic has subsided, Affirm shares have taken a hit, falling sharply from their 2021 peak of nearly $170. Year-to-date, Affirm shares are down 31%.

In a major development announced this month, Affirm has partnered with Apple. As part of the partnership between the two companies, Apple will discontinue its “buy now, pay later” service later this year and use Affirm as a third-party app for installment loan purchases.

The company’s overall strength can be seen in its latest earnings report. Affirm reported fiscal 3Q24 revenue of $576 million, up more than 51% year-over-year and beating estimates by more than $26 million. Ultimately, the company reports a net loss, but in this latest report, the EPS net loss of 43 cents wasn’t as deep as expected, beating estimates of 28 cents per share.

Affirm’s combination of strong performance and smart management caught the attention of Goldman’s Ng, who wrote of the company: “We are particularly impressed by AFRM’s underwriting sophistication compared to other fintechs and the company’s strong track record of achieving well-managed credit results despite faster growth than peers… We believe this, combined with the secular tailwinds favoring BNPL and Pay-in-4 offerings and AFRM’s impressive distribution with major credit platforms e-com, should lead to strong market share gains and provide a path towards AFRM becoming one of the first new closed-loop platforms in the payments ecosystem.”

Looking ahead, Ng is also impressed by the potential of Affirm’s various partnerships, writing, “AFRM is still small in the grand scheme of unsecured lending in the U.S., and we see the company’s partnerships with Shopify, Amazon, Walmart, and most recently Apple Pay as important unlocks that should allow the company to maintain high growth rates.”

Quantifying this position, Ng rates AFRM shares a Buy and his price target, set at $42, implies a one-year upside of ~34%. (To see Ng’s resume, Click here)

While Goldman’s view is quite bullish, Wall Street’s overall view of AFRM is more cautious. The stock’s consensus rating is Hold, based on 14 recent analyst reviews that break down into 4 Buys, 7 Holds, and 3 Sells. The shares are currently trading at $30.46 and the average price target of $37.44 suggests an upside of ~23% over the next year. (See AFRM Stock Forecast)

To block

Next up is Block, one of the biggest names in fintech. The company started out as Square, the merchant-facing payment processor, but as it expanded, it transformed into a holding company. Under the Block name, the company continues to own and operate Square; its other major subsidiary is Cash App, the popular digital payment app.

Between them, Block’s two largest subsidiaries lend a helping hand to the company on both sides of the digital transaction landscape. Merchants use Square for efficient process automation, revenue stream organization, and payment acceptance flexibility, all to smooth and increase their revenue stream. Square’s app includes software that can be accessed via smartphones and tablets, as well as hardware that can turn handheld devices into cash registers and card readers. Cash App lets its users quickly streamline their cash account, for fast, easy, and most importantly, universally accessible online payment options.

Even though shares are down 18% this year, sales are up. Block’s 1Q24 revenue was $5.96 billion, up more than 19% year-over-year, beating expectations by $140 million. These solid revenues supported earnings, by non-GAAP measures, of 85 cents per share, 12 cents per share ahead of forecast. The company’s gross profit was $2.09 billion, up 22% from the prior-year quarter. Subscriptions and services were among the main drivers of this successful quarterly report; S&S’s revenue increased 23% y/y to $1.68 billion, while its gross profit grew 28% y/y to $1.41 billion.

Analyzing Block for Goldman, analyst Ng sees a solid fintech with great potential. He writes in his recent note: “We view SQ as one of the leaders in SME payments and consumer fintech, capitalizing on its long history of product-led innovation. Excluding COVID years, shares remained range-bound for 6 effective years, despite a 44%/22%/41% CAGR on Gross Profit/Seller GPV/Cash App Assets. Additionally, the company has also begun increasing free cash flow and valuation support, introducing a Rule of 40 framework, moving to GAAP-based targets (including SBC), and still expects mid-teens GP growth.

Ng goes on to outline the future path of this company, painting a picture that should interest investors: “By our estimates, the shares are trading at approximately 18 times our GSe adjusted EPS estimate for 2025, which we think is attractive for a company that will continue to grow its market. double-digit top-line and with several “moon shot” levers to accelerate growth.”

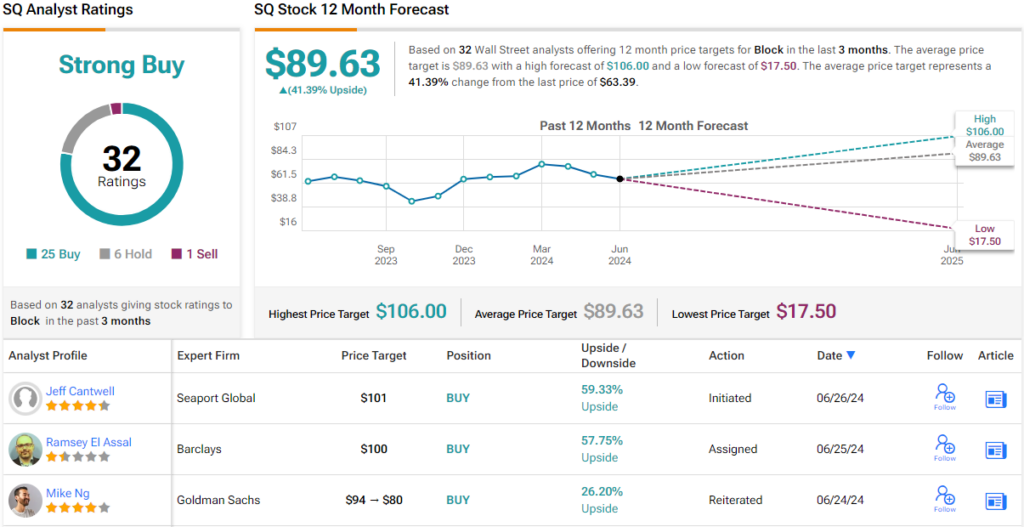

Overall, Ng rates SQ shares a “Buy,” while his $80 price target implies a 26% upside over the one-year horizon.

This view from Goldman is not unusual, and Block’s Strong Buy consensus rating is based on 32 recent reviews that include 25 Buys, 6 Holds, and just 1 Sell. The company’s shares are selling for $63.39 and have an average price target of $89.63, which is significantly more bullish than Goldman’s and indicates a one-year earnings potential of 41%. (See SQ Stock Forecast)

To find good ideas for trading fintech stocks at attractive valuations, visit TipRanks Best stocks to buya tool that unites all of TipRanks’ stock information.

Disclaimer: The views expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.