Fintech

Mobile Money and FinTech Innovation in Sub-Saharan Africa

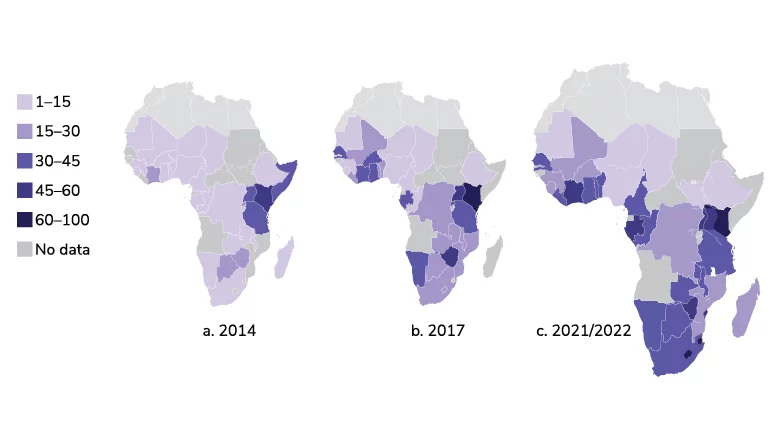

In sub-Saharan Africa, mobile money is now essential to promoting financial inclusion. Thanks to innovative mobile network operators in Kenya and elsewhere, East Africa used to be the hub of mobile money.

The availability of these services has expanded recently, to the point that by 2022 all 12 of the world’s economies will be located in sub-Saharan Africa, and there will be more adults with mobile money accounts there than with bank or other similarly regulated financial institution accounts.

In 2022, 28% of the adult population in sub-Saharan Africa had an average mobile money account. Although mobile money is not yet widely accepted in some economies, it is more of a minority than a common occurrence.

In 20 of the 36 economies studied, at least 30% of the population has mobile money accounts. Considering that 13% of people in emerging economies have mobile money accounts on average, this is even more impressive.

Reaching the unbanked population

The region’s economic landscape, which relies heavily on cash transactions in informal markets, has posed challenges for banking services to adapt. In 2022, more than two-thirds of payments by individuals in South Africa were made in cash, despite 85% of the population having a bank account. Meanwhile, additional challenges, including concerns about fraud, payment delays and relatively low financial literacy, are hindering the growth of banks across the region.

Mobile money is effectively addressing these issues. These services offer simplified procedures for getting started and logging in via Unstructured Supplementary Service Data (USSD), an encoded mobile communication protocol that relies on text messages rather than an Internet connection.

They are supported by 2G and 3G networks that serve over 80% of the population in the area. Major telecom companies are supporting the launch of mobile money services, offering greater security, convenience and instant transactions.

A push towards cashless transactions

Mobile money services have evolved from peer-to-peer (P2P) transactions to cash-in and out transactions, enabling the purchase of goods and services as demand grows and operators continue to innovate.

More unbanked people can rely on online mobile money transactions thanks to increased internet penetration and the introduction of affordable smartphones. This has led to a 29% increase in e-commerce value growth in Sub-Saharan Africa by 2022.

Mobile money opens up new avenues for understanding consumer trends and simplifying payments. B2B and B2C companies have used transaction analytics to improve customer experiences, develop targeted marketing strategies, and build brand loyalty.

Telecoms are driving growth, but fintech will become more important

Fintechs will become more significant, but telecom companies will likely continue to drive growth in consumer electronic payments. In Africa, mobile money has completely changed the way consumers shop.

By introducing cutting-edge payment solutions and other value-added services to their sizable customer base, telcos have played a significant role in driving the expansion of payments in Africa over the past decade through mobile money.

This pattern is expected to persist. Consumers have already moved from basic mobile money (Wallet 1.0), which primarily provided incoming and outgoing money and peer-to-peer (P2P) transfers, to Wallet 2.0, which offers more comprehensive financial services such as bill payments, savings, loans, and insurance.

Wallets 2.0 are starting to show signs of improvement, wallets 3.0 will be feature-rich wallets with access to services, in-app purchases, and connection to online retailers, marketplaces, and platforms as a payment option in addition to basic financial services.

Small Businesses Get a Boost from FinTech

An estimated 80-90 million SMEs in Africa still represent a huge unrealized potential in the payments industry. The recent growth in African payments has been largely attributed to FinTech innovation, merchant acquisitions, and related offerings.

Specialized FinTech consulting firms will be at the forefront of helping small and medium-sized businesses transition from traditional offline sales to online e-commerce, as reported by 37% of survey participants. The survey predicts that within three years, at least 25% of SMBs will have a digital footprint.

A driving force for FinTech innovation

Mobile money is becoming a driver of innovation as central banks lower barriers to entry into the financial sector, creating space for diverse revenue streams through new services such as insurtech and microcredit. Orange Bank Africa has used this opening to introduce nanocredit in Côte d’Ivoire.

By 2025, the company hopes to have provided these loans to 10 million customers in Senegal, Mali and Burkina Faso. In line with this, MTN partnered with Sanlam in 2022 to expand access to Ayo Insurance, a reasonably priced microinsurance program for the self-employed and informal workers in Ghana, Uganda and Zambia via mobile money services. By 2025, the strategic alliance hoped to reach 30 million users.

Adoption of mobile money poses consumer protection risks

Any initiative to increase financial inclusion through the use of digital connectivity and mobile money accounts should be complemented by initiatives to safeguard consumers. Digital skills are needed for digital financial services such as mobile money. These include the ability to manage passwords, activate digital wallets or accounts, transit user interfaces and use authentication systems.

Consumer concerns include lack of clarity about fees and other terms of service, aggressive marketing, inadequate dispute management, identity or data theft, mobile app fraud, and other dangers. These risks are not new; bank accounts already have them, but the accessibility and ease of use of mobile money have made them more significant.

For example, according to Global Findex 2021, a significant portion of account holders who had their paychecks deposited directly into their accounts faced unexpected fees. Of these adults, 5% in Cameroon reported having to pay surprise fees. We’re not sure if these were unofficial fees or if the user simply didn’t understand the charging schedule, but both scenarios suggest there may be room for abuse. Women may be more susceptible to unexpected fees and other types of exploitation since they often lack prior financial knowledge.

Conclusion

In Sub-Saharan Africa, supervisory agencies and financial regulators need to strengthen supervisory monitoring systems to detect and measure the many financial risks prevalent in the market, especially with the growing use of mobile money. It is equally critical to oblige providers to take action to ensure that mobile money users understand all product features and fee disclosures.