Fintech

SoFi and Pagaya: Jefferies Picks the Best Fintech Stocks to Buy Before Earnings

Despite recent losses, the tech-heavy NASDAQ remains up nearly 16% year-to-date. With tech showing solid growth, it’s a good time to explore tech stocks, especially in specialized areas like financial technology.

Fintech exists at the nexus of banking and high-tech. Fintech companies provide a wide range of banking services, including checking and savings accounts, lending and borrowing, money management, and even investments, all offered online, including on mobile devices. From the customer’s perspective, fintechs offer the convenience of banking anywhere, anytime, without the high overhead of operating physical branches.

Covering fintech for Jefferies, 5-star analyst John Hecht noted, “Fintech stocks outperformed this quarter as industry trends and evolving rate expectations were net positives. Origination volumes stabilized, lenders remained cautious given elevated (but stable) DQ formation and slowing consumer spending, while funding markets remained supportive for issuers.”

In this context, we used the TipRanks database to seek a broader view of the market on SoFi (NASDAQ:SOFI) and Pagaya (NASDAQ:PGY), two of Hecht’s “Buy” picks in his note. The Jefferies analyst advises investors to buy into these stocks ahead of their upcoming earnings reports; let’s take a closer look and find out why.

SoFi Technologies

The first fintech we’ll look at is SoFi, which gets its name from its niche: social finance. SoFi incorporates the interactive online experience of social media into fintech and digital banking.

SoFi is licensed as a bank, and its customers can access the usual banking services, take out personal, home, or auto loans, open credit card accounts, invest money, hold savings or checking accounts, refinance, or cancel existing third-party debt such as student loans. The company describes itself as a “one-stop shop” for personal finance and boasts more than 8 million members.

The company has funded more than $73 billion in loans for its customers, who have paid off approximately $34 billion in personal debt and earned more than $34 million in personal rewards. As a licensed bank, SoFi is covered by the FDIC, and members’ personal checking and savings accounts are protected up to the standard level of $250,000.

For the first quarter of 2024, SoFi reported a total of 8.132 million members, reflecting a quarterly gain of 622,000 and a 44% increase year-over-year. Although the company’s revenues fell from Q4 to Q1, they still came in just under $581 million, marking a 26% increase year-over-year and beating estimates by more than $21 million. SoFi also posted GAAP earnings of 2 cents per share, beating estimates by a penny.

Looking ahead to Q2 earnings, we find that most analysts are expecting earnings of $0.01 per share, based on revenues that could approach $566 million. Hitting that level of revenue would equate to a 15% year-over-year gain. SoFi’s Q2 earnings call is scheduled for the morning of July 30.

Turning to Jefferies’ view, senior analyst Hecht writes: “2024 remains a transition year for SOFI with an overall more conservative lending position. That said, management is bullish on the Tech and Money segments and expects 20% and 75% growth, respectively. Management expects the segments combined to contribute more than 50% of total revenue in FY24…”

Hecht goes on to outline his thoughts on SoFi’s likely results and what investors can expect, adding, “Our EPS of $0.01 is in line with Wall Street. We expect 2Q24 adjusted net sales of $560 million, at the midpoint of $555-565 million guidance. This translates to 15% year-over-year growth, driven by loan receivables growth of ~29% year-over-year coupled with higher yields, along with expected growth from the technology platform. We are expecting adjusted EBITDA of $120 million, at the midpoint of $115-125 million guidance, and net income of $6 million, which is toward the lower end of $5-10 million guidance.”

These comments inform Hecht’s Buy rating on the stock, and his $12 price target implies about 61% upside over the next year. (To look at Hecht’s track record, Click here)

The rest of the Street is less confident, however; based on 4 Buys, 9 Holds, plus 3 additional Sells, the stock has a consensus rating of Hold (aka Neutral). Shares are selling for $7.47, and the average price target of $8.15 suggests the stock has 9% upside potential in a year. (See SOFI Stock Forecast)

Pagaya Technologies (PGY)

The second fintech on our radar now is Pagaya, a company that is applying AI technology to the credit system. In short, Pagaya uses AI and machine learning methodologies, along with big data analytics, to give institutional lenders new and more accurate ways to review credit applications. The company works with a wide range of financial institutions, including banks, pension funds, and insurance companies, applying data-driven decision-making to improve people’s access to credit.

At its core, Pagaya aims to fill in the blind spots that legacy underwriting systems miss. The company has an AI network that analyzes credit applications and credit applicants to provide more precise risk assessments for better risk management. The company, founded in 2016, operates internationally, with a suite of 30 partners and employs over 600 people, including top data scientists. Since its founding, Pagaya has reviewed approximately $2 trillion in credit applications.

Pagaya shares have been on a downward trajectory over the past year; the stock is down 45% over the past 12 months. At the same time, Pagaya’s revenue has been on an upward trajectory over the past few quarters. The company’s 1Q24 revenue came in at $245 million, up 31% year over year and $17.23 million above estimates. The company’s bottom line, non-GAAP earnings of 20 cents per share, were 4 cents better than expected. In other positive metrics, the company’s Q1 net volume was a company record, at $2.42 billion, and $20 million in cash flow from operations marked the third consecutive quarter of positive cash generation.

Forecasters expect Pagaya to report $239 million in revenue in Q2, with EPS of 28 cents per share. Q2 results are due on August 9.

For Hecht, a key takeaway here is Pagaya’s recent growth. He says of the fintech company, “Pagaya remains on a strong growth trajectory. Management reiterated its plan to add 2-4 new lending partners annually. Growth areas include its auto and POS businesses, and we expect PGY to lean into them as the year progresses. Investor focus in the quarter remains on PV brands and the company’s capital efficiency (with respect to increasing ABS retention).”

Continuing, the analyst adds of Pagaya’s likely Q2 results, “For the quarter, we expect adjusted EPS of $0.29 versus the Street’s adjusted EPS forecast of $0.24… We expect net volume of $2.3 billion, the midpoint of the company’s forecast for the quarter. Our total revenue and other income forecast of $237.9 million aligns with the Street’s $238.9 million and is within the company’s forecast for the quarter… Our 2Q24 adjusted EBITDA forecast is $42.7 million, which is within guidance, and our FY24 forecast remains at $173.5 million.”

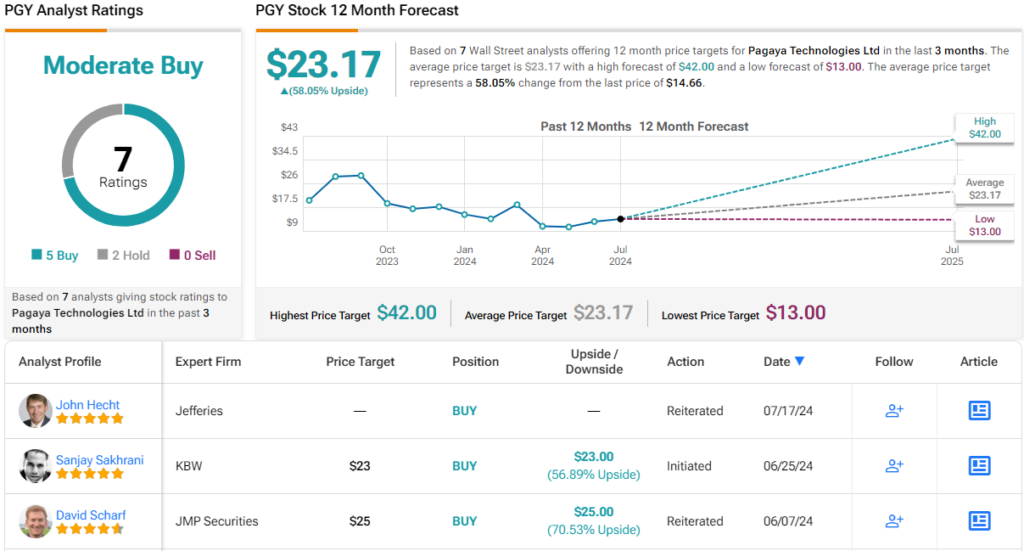

Along with this optimistic outlook, Hecht gives PGY shares a Buy rating, with a $30 price target that suggests a solid 109% gain in the coming months.

All in all, Wall Street rates PGY a Moderate Buy, based on 7 reviews including 5 Buys and 2 Holds, and the average price target of $23.17 suggests a 58% upside over the one-year horizon. (See PGY Stock Forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best stocks to buya tool that unites all of TipRanks’ stock insights.

Disclaimer: The views expressed in this article are solely those of the featured analyst. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.