Fintech

SoFi: Rising Longer Is An Advantage, Along With Fintech Diversification (NASDAQ:SOFI)

Dilok Klaisataporn/iStock via Getty Images

We have already covered SoFi Technologies (NASDAQ:SOFI) in February 2024, discussing why we maintained our Buy rating, with the online bank likely to continue generating excellent results as management initiated the growth trend for the credit/technology segment.

Combined with the growth in bank deposits, the contribution to lower cost financing, the promising turnaround in its GAAP profitability and the decline in the share price, we had maintained our Buy rating then.

Since then, SOFI has unfortunately retreated another -13.1%, well underperforming the broader market at -2.5%. Nonetheless, we maintain our Buy rating, thanks to promising top-line and bottom-line growth as management implements dual growth as both an online bank and a fintech.

At the same time, investors should also temper their near-term expectations, with the stock likely to move sideways until the company achieves substantial GAAP EPS profitability and the credit/technology segment emerges as the top/bottom line driver .

SOFI’s investment thesis remains strong, although the market likely needs some convincing

For now, SOFI reported a double FQ1’24 earnings forecast, with revenues of $580.64 million (-2.1% QoQ/ +26.3% YoY) and an adjusted EBITDA of $144.38 million (-20.4% QoQ/ +89.4% YoY), implying rich adjusted EBITDA margins of 24, 8% (-5.6 QoQ points/ +8.4 YoY).

Much of the top-line and bottom-line benefits are attributed to the robust growth seen in the online bank’s net interest margin to $402.71 million (+3.3% QoQ/+70.6% YoY) and in net interest margins at 5.91% (-0.11 quarterly points/+ 0.44 on an annual basis).

With interest rates still high, it is no surprise that management has been able to generate excellent spreads from its members’ savings balances with an annual percentage yield of 4.60%, while the deposit base rises to $21.6 billion (+16.3% QoQ / +116% YoY).

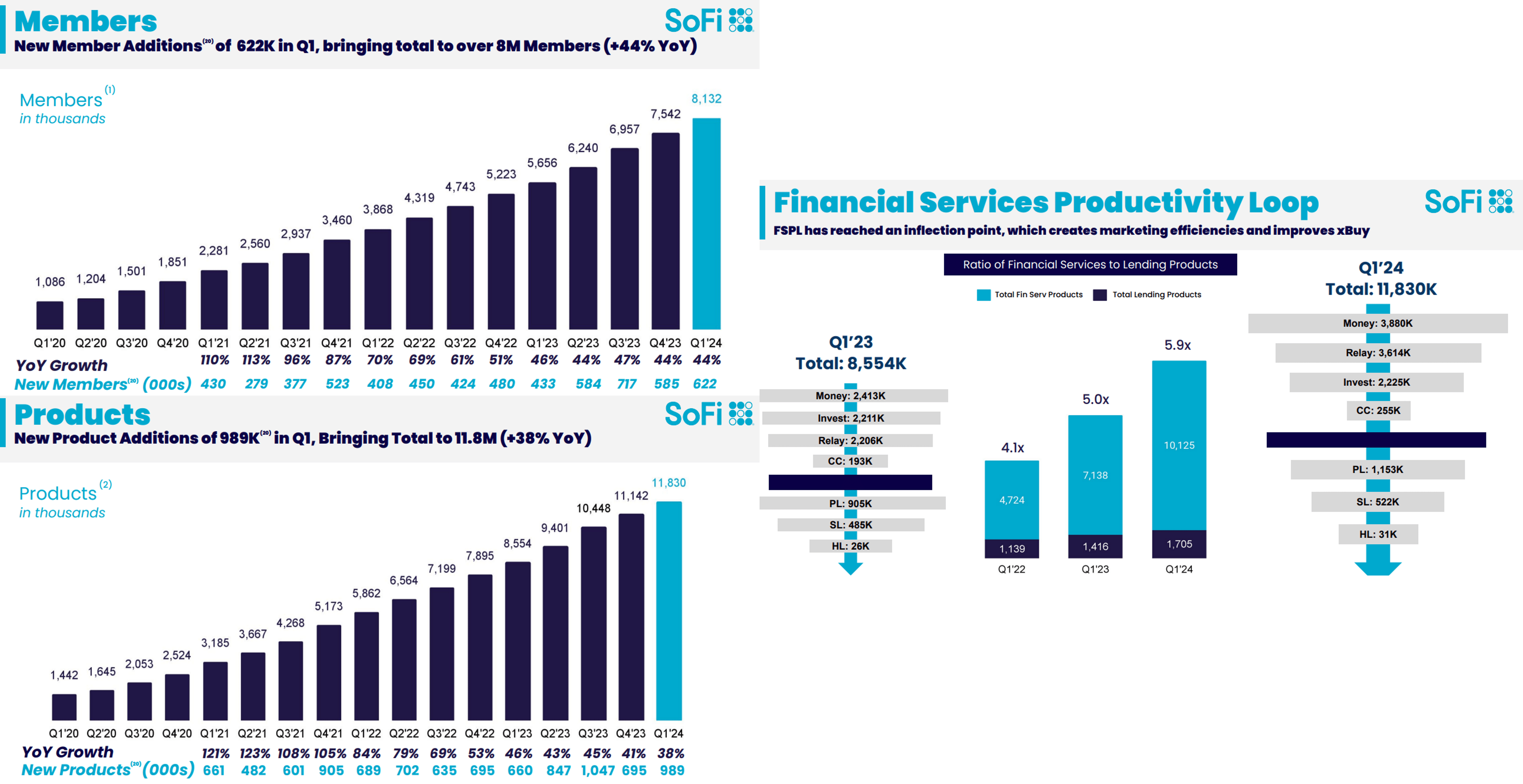

SOFI’s growing Fintech segment

SOFI

At the same time, driven by growth in SOFI membership and increased cross-selling/products sold in the financial services and lending segment, it reported accelerating non-interest income of $242.27 million quarter-on-quarter in the first quarter of 2024 (+7.3% on a quarterly basis / +2.5% on an annual basis).

More importantly, the Financial Services/Technology Platforms segment also comprises a growing share of its revenues, accounting for 42% in Q1 2024 (+2 points QoQ/ +9 YoY), naturally diversifying the revenue stream, being “on track to finish 2024.” with a revenue mix close to 50:50.”

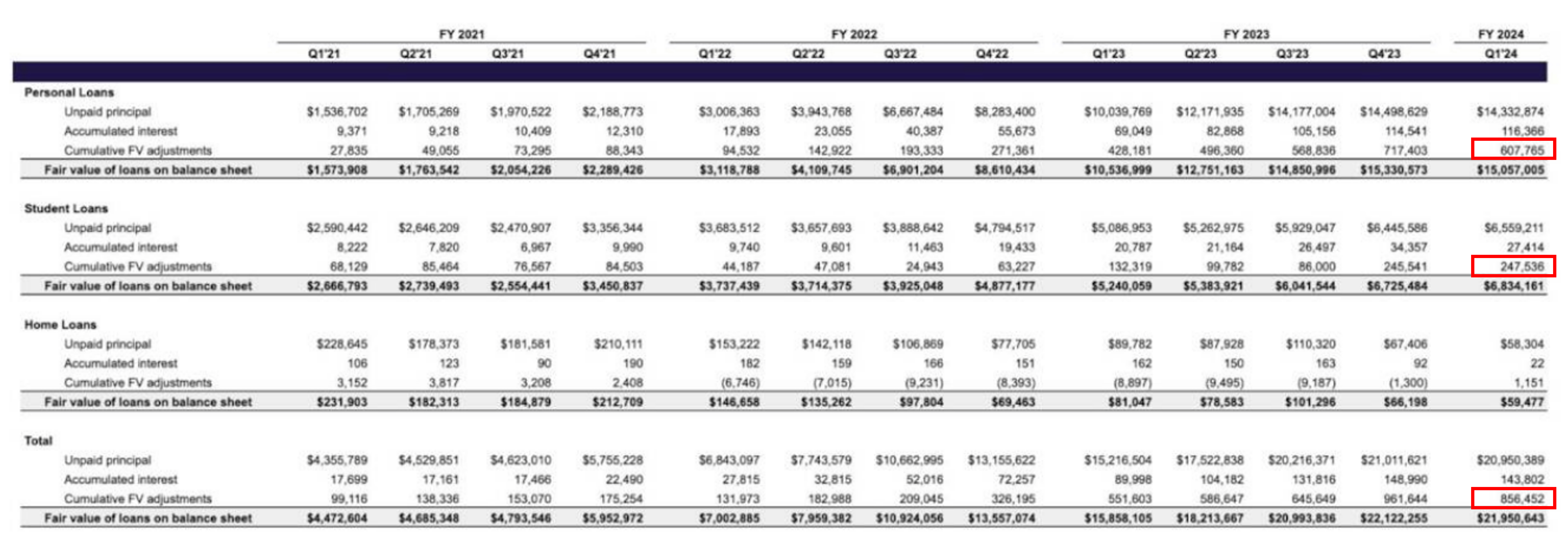

SOFI default rates

In search of the Alpha

After eight consecutive quarters of increasing loan delinquencies, it appears that the situation has started to moderate for SOFI as well, with a decline in “cumulative fair value adjustments” of 3.9% (-0.4 quarterly points/+0.6 on an annual basis) to $856.45 million in the first quarter. 24 (-10.9% on a quarterly basis/ +55.3% on an annual basis).

With the US job market still robust, it appears that consumers remain sufficiently liquid, further aided by the borrower complex Weighted average issue FICO of 750 in March 2024.

This also explains why SOFI moderately increased its guidance for fiscal 2024, with financial services net revenue growth of at least +75% y-o-y and technology platform growth of +20% y-o-y in the fiscal year 2024, compared to the original mixed guidance of +50% y-o-y. for the overall technology platforms and financial services segment.

This is in addition to improved financial guidance for fiscal 2024, with higher adj EBITDA of $595 million (+37.8% YoY), adj EBITDA margins of 24.6% (+4.3 points YoY) and GAAP EPS of $0.08 (+122.2% YoY), compared to the original forecast of $585 million (+35.5% YoY), 24.5% (+4.2 points YoY) and $0, 07 (+119.4% YoY), respectively.

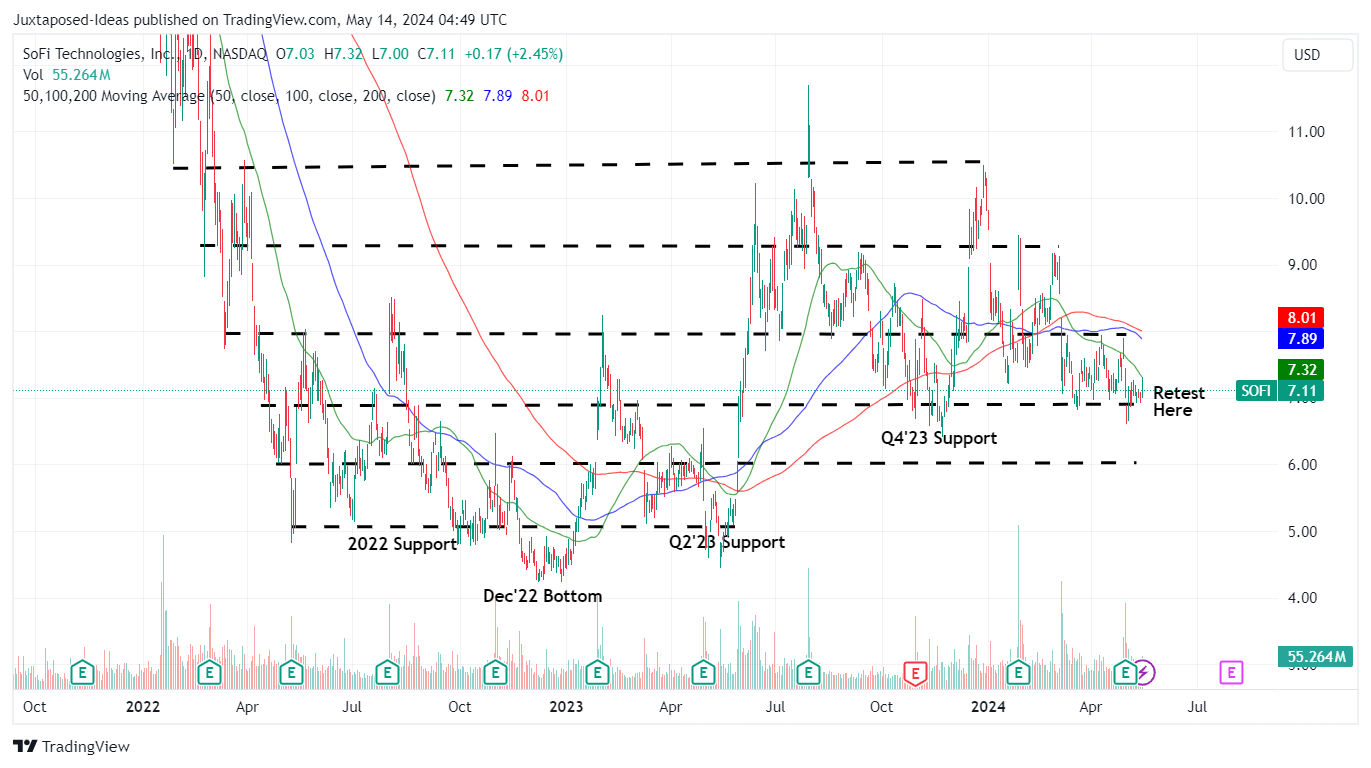

SOFI 2Y stock price

TradingView

Despite this, SOFI has already lost much of its 2024 gains, trading below its 50/100/200-day moving averages and vastly underperforming the broader market.

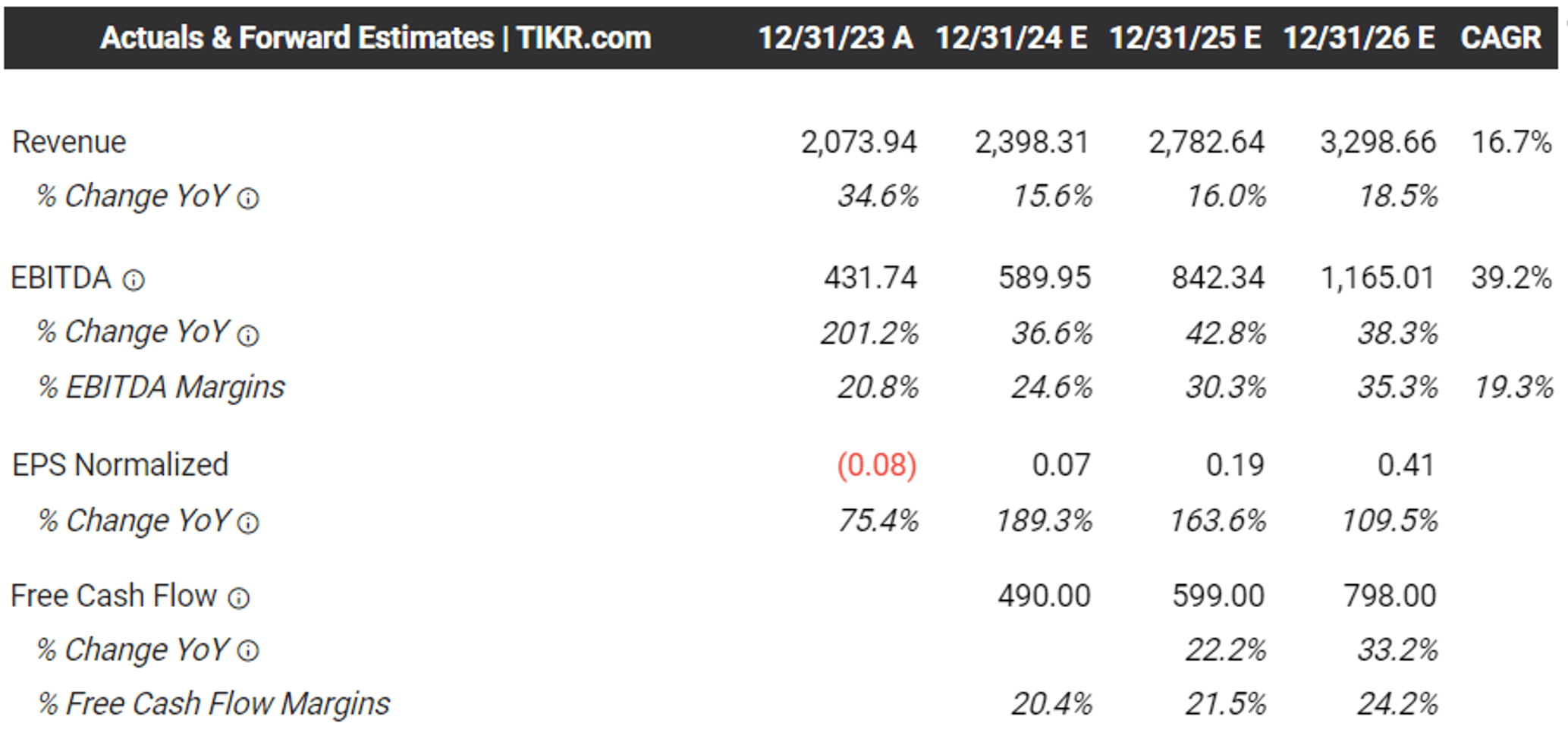

Future consensus estimates

TIKR terminal

With minimal adj EPS profitability, for now we’ll look at SOFI’s adj EBITDA. Based on enterprise value of $6.14 billion at the time of this writing and adjusted EBITDA of $500.41 million generated over the course of LTM (+137.9% sequential) and consensus estimates of above, it appears the stock is trading at a LTM EV/EBITDA of 12.26. x and FWD EV/EBITDA of 8.57x.

Comparing SOFI’s FWD Price/Sales of 3.06x and FWD EV/EBITDA of 8.57x to its fintech/lending/digital wallet competitors, such as Block (m2) at 1.75x/ 15.44x, PayPal (PYPL) at 2.06x/ 10.35x, Upstart (UPST) at 4.14x/ NA and Affirm (AFRM) respectively at 4.32x/NA, it is clear that the former has been discounted here.

This is primarily because SOFI is expected to generate impressive top-line and bottom-line expansion at a CAGR of +16.7%/+39.2% through fiscal 2026, building on historical growth of +43 %/+278% between fiscal 2021 and fiscal 2023, respectively.

SOFI numbers have also accelerated significantly, when compared to the forecast growth of SQ at +11.8%/+35.1%, PYPL at +7.7%/-1.5%, UPST at +19.1 %/NA and AFRM at +26.6%/NA over the same time period respectively.

We believe SOFIs can continue to enjoy robust profit tailwinds from higher interest rates for a longer period as inflation remains sticky, likely to boost the online bank’s net interest income before the Fed changes course and before the macroeconomic context normalizes. in the next years.

Combined with management’s stepped-up efforts in the lending and financial services segment, as noted in the updated fiscal 2024 guidance above, we believe SOFI could very well emerge as a winner in the online banking/fintech market, strengthening its robust growth prospects.

So, SOFI stock is a buySell or Keep?

Thanks to the attractive risk/reward ratio, we maintain our Buy rating for SOFI, albeit without a specific entry point as it depends on the individual investor’s dollar cost average and risk appetite.

With the stock currently retesting its H2’23 and H1’24 support levels of $7, interested readers may want to watch its movement a little longer before adding whether this level holds.

It goes without saying that SOFI is only suitable for those with a higher risk tolerance, attributed to the fintech’s slower GAAP EPS profitability, high short interest of 18.6% at the time of this writing, and the enormous volatility of the title from the beginning of 2021.

At the same time, we believe the stock will likely continue to be discounted until its fintech segment emerges as the driver of earnings and profits, with its long-term outlook now overly skewed towards online banking.